When it comes to saving for your child’s college education, knowing how much you should have saved at each stage of their life can help ensure you’re on track. The 529 plan is a popular savings tool, but how much should you be contributing, and at what point should you expect your balance to grow? Let’s break it down in a manageable way, using a realistic target based on the child’s age and the typical growth pattern of a 529 account.

Understanding the 529 Plan

A 529 plan is a tax-advantaged savings account designed to help families save for education expenses. Contributions grow tax-deferred, and withdrawals used for qualified education expenses are tax-free. However, the amount you need to save will vary depending on when you start and your savings goals. The earlier you begin saving, the more time your investment has to grow, thanks to compound interest.

Here’s an easy guide to understanding how much you should ideally have saved in your 529 plan at different ages, based on a typical range of growth.

Projected Savings for Each Age

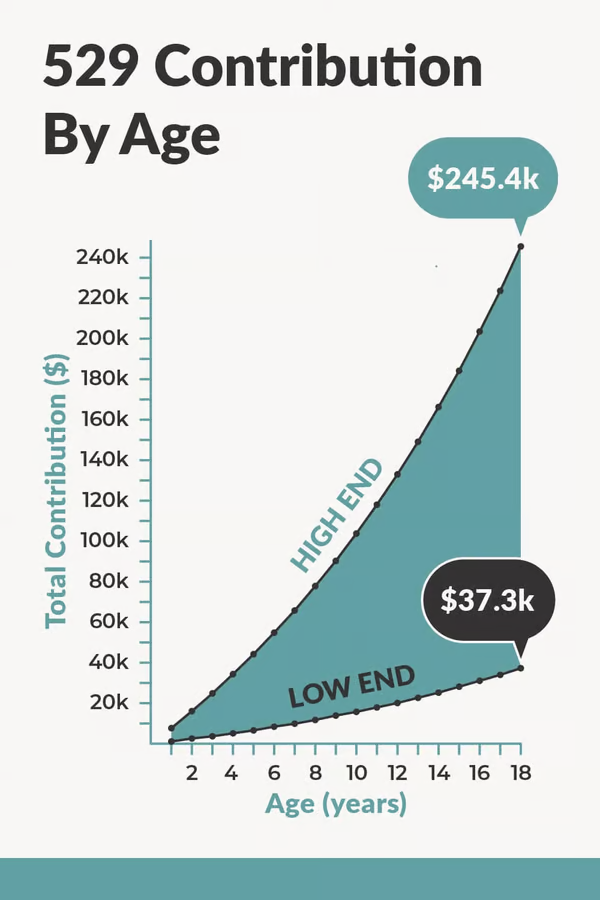

To give you an idea of how much you should have in your 529 plan by the time your child reaches certain ages, we’ve outlined the low-end and high-end savings estimates. These numbers assume a steady contribution over time, with growth based on a typical investment return.

Age 1:

- Low End: $1,189

- High End: $7,816

Starting early can really make a difference. Even at age 1, your 529 plan can begin to accumulate funds with small but consistent monthly contributions.

Age 2:

- Low End: $2,451

- High End: $16,144

At this point, your child’s 529 account should be growing steadily, especially if you started contributing early and let the power of compounding work for you.

Age 3:

- Low End: $3,791

- High End: $24,923

With three years of savings, the account balance continues to rise. If you’ve been regularly contributing, you’re setting a strong foundation for college savings.

Age 4:

- Low End: $5,213

- High End: $34,276

By the age of four, the savings should be growing more rapidly, with a noticeable increase from previous years.

Age 5:

- Low End: $6,723

- High End: $44,206

Five years in, and the benefits of compounding are becoming clearer. Your contributions are now being matched with more growth, pushing the balance even higher.

Age 6:

- Low End: $8,327

- High End: $54,749

The amount in your 529 plan has started to gain significant momentum, thanks to the continued contributions and investment growth.

Age 7:

- Low End: $10,029

- High End: $65,941

Your child is now seven, and the account is growing steadily, nearing the $10,000 mark in the low-end estimate. You’re on track for more substantial savings by the time they enter high school.

Age 8:

- Low End: $11,836

- High End: $77,824

As your child continues to grow, your contributions and the account’s growth should continue to compound effectively, allowing you to reach nearly $12,000 in savings by age 8 on the lower end.

Age 9:

- Low End: $13,755

- High End: $90,440

At this point, your savings are starting to accumulate rapidly, providing a solid cushion for future college expenses.

Age 10:

- Low End: $15,792

- High End: $103,834

With a decade of savings, you should have a substantial amount saved in the 529 plan. As the balance grows, it will continue to have a positive impact on your ability to meet your college funding goals.

Age 11:

- Low End: $17,955

- High End: $118,054

You’re getting closer to high school, and your 529 plan should reflect the progress of your consistent savings and investment strategy.

Age 12:

- Low End: $20,251

- High End: $133,151

By age 12, your 529 account should be seeing considerable growth, bringing you closer to covering a significant portion of college expenses.

Age 13:

- Low End: $22,689

- High End: $149,179

As your child enters their teenage years, the amount of money saved for their college education continues to climb. The next few years are crucial for maximizing your savings.

Age 14:

- Low End: $25,277

- High End: $166,196

With just a few more years until high school graduation, your 529 plan should be ramping up, providing a strong foundation for the upcoming years of college funding.

Age 15:

- Low End: $28,025

- High End: $184,263

At 15, the 529 balance should be nearing a significant portion of the projected total cost of a public university education.

Age 16:

- Low End: $30,942

- High End: $203,444

Your child is getting ready for their final years at home, and your contributions are helping pave the way for their college years.

Age 17:

- Low End: $34,039

- High End: $223,807

The finish line is in sight. At this point, your 529 savings are approaching the amount needed for a significant portion of college costs, depending on the type of school they attend.

Age 18:

- Low End: $37,328

- High End: $245,427

By the time your child turns 18, your 529 plan should be fully set up to pay for their college expenses, especially if you’ve been diligent about saving.

Managing Expectations

While these numbers can seem daunting at first, remember that they are based on regular monthly contributions and an average return on investment. You don’t need to save 100% of the costs upfront; your child can contribute through scholarships, part-time jobs, and student loans.

Additionally, each state has different tuition rates and a variety of options for how you can invest in a 529 plan. The Fidelity college savings calculator can help you determine a more personalized savings goal based on your child’s future college costs.

Conclusion

Saving for college doesn’t have to be overwhelming. By understanding how much you should have saved at different stages of your child’s life, you can develop a manageable and strategic savings plan. Start early, save consistently, and take advantage of the benefits offered by 529 plans to make college a more affordable reality for your child.

{kind=link}